Buying a house is an exciting milestone, but it also comes with a complex and sometimes overwhelming process: the process of closing on a house. Understanding this process is crucial to avoid surprises and ensure a smooth closing. In this comprehensive guide, we'll walk you through each step, from preparing for the process of closing on a house to signing the final documents and help you make informed decisions along the way.

Prepare for closing to ensure a successful transaction, including obtaining mortgage pre-approval and opening an escrow account.

Verify ownership of the property and obtain title insurance during the title search process.

Engage professional assistance throughout the entire closing process to protect your interests.

Preparing for closing is essential to ensure a smooth process and avoid surprises. Mortgage pre-approval, opening an escrow account and understanding the paperwork are all important steps. Not only does proper preparation save you time, but it also prevents any unexpected issues from arising during the closing process.

Due diligence is a critical aspect of preparation, as it involves thoroughly examining a property to guarantee that there are no unexpected surprises. Analyzing the neighborhood and environment and reading the Seller's Disclosure can provide insight into any major issues that may not have been identified during the final inspection. Consult with your loan officer if you have any concerns about the property.

An escrow account is a third-party-held account that securely stores money and documents related to a transaction until all terms of the agreement are fulfilled. This account plays a crucial role at the closing table when finalizing the purchase of a house. Escrow agents, who can be escrow companies, title companies or real estate attorneys are responsible for retaining the earnest money.

When opening an escrow account it is important to include the account details in the purchase contract for the home. Additionally, the escrow agent may require a cashier's check or wire transfer to deposit the earnest money in a real estate transaction.

A title search is the process of verifying ownership and claims on a property thus ensuring that the seller has the legal right to sell the property to you. A title company conducts this search and plays a crucial role during the closing process.

Title insurance provides protection against potential financial losses resulting from any defects in the title. It's important to obtain title insurance to safeguard your investment and avoid potential financial complications due to unforeseen issues with the property's title.

The payment for the lender's policy for title insurance is subject to state laws and the outcome of negotiations between the buyer and seller.

Obtaining professional help for closing on a house is significant as it can guarantee that all requisite documents are accurately prepared and submitted, which can help avert delays or legal issues during the closing process. It can also provide direction on any queries or apprehensions that may arise during the process.

Hiring a real estate attorney is optional but advisable for understanding and reviewing the complicated jargon in closing documents. A real estate agent can also facilitate contact with home inspectors, attorneys, title companies and other relevant professionals hopefully ensuring that you have the necessary support throughout the closing process.

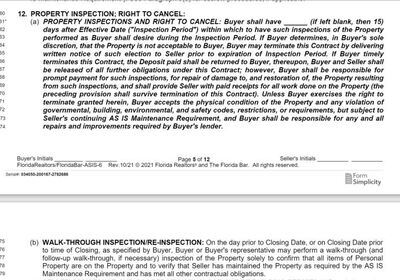

Home inspection and pest inspection are necessary steps in the closing process to identify potential problems with the property. A home inspection evaluates a home and its systems, while a pest inspection is a specialist examination to ensure that a home is free of wood-destroying insects, such as termites or carpenter ants.

If a home inspection report indicates any significant issues, the buyer should weigh the risk of continuing with the purchase and consider obtaining a seller's concession. Failure to submit repair requests in a timely manner will result in the forfeiture of the right to ask for repairs.

Negotiating closing costs is crucial to prevent snowballing fees, including unexpected junk fees that can be reduced or eliminated by speaking up. Junk fees are additional charges imposed by the lender at the time of closing a mortgage. These expenses may not be properly communicated to the borrower.

If a major issue is identified during the inspection that the seller is unable or unwilling to address, it is possible to withdraw from the agreement without penalty. Including an inspection contingency in the purchase contract and making a decision within the allotted timeframe, buyers may choose to terminate the contract and receive their earnest money back.

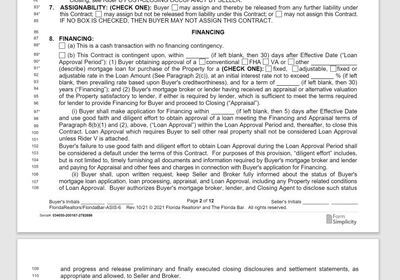

Securing your mortgage and interest rate is important to avoid market fluctuations and potential rate hikes that could increase monthly payments and repayment time. The property is under contract, now you can avail the opportunity to lock in your desired mortgage rate with a reliable mortgage lender. This can be done at the right time to successfully secure the mortgage of your choice. If you anticipate closing outside of the specified time frame, you may be able to obtain a rate-lock extension.

A rate lock is a guarantee from the lender that the interest rate will remain constant during the loan approval process, which includes providing a loan estimate. It is essential to lock in your interest rate to prevent potential market variations and rate increases that could lead to higher monthly payments and an extended repayment period.

A float-down provision stipulates that if interest rates decrease during the lock period, the borrower will be eligible for the lower rate.

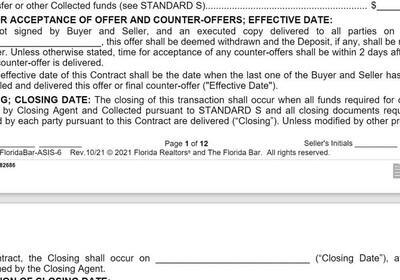

Contingencies in real estate offers are conditions that must be satisfied in order for the sale to proceed. Active approval of contingencies refers to the procedure of formally removing contingencies through written documentation by the dates stipulated in the purchase offer, while passive approval implies that the buyer does not express any objection to the contingencies by the designated deadlines and they are deemed to be approved.

Buyers must be cognizant of the approval process and adhere to the necessary deadlines for taking the appropriate actions. Including contingencies like home inspection or financing can protect your interests and provide you with more flexibility during the closing process.

The final walk-through serves as an opportunity for the buyer to inspect the property for any damage, confirm that required fixes have been completed, and verify that nothing in the purchase agreement has been removed prior to signing closing papers. During this walk-through, it is important to ensure that the property is in accordance with the details stipulated in the contract and to inspect appliances, toilets, doors, windows and light fittings.

If something is amiss during the final walk-through, the agent will notify the seller's real estate agent of the issue. After the final walk-through, the earnest money in the escrow account will be allocated toward the down payment on the home.

Reading and understanding the legal paperwork, including the closing disclosure, during the closing process is crucial due to legal jargon and financial impact. The title agent or attorney handling the closing is responsible for elucidating the nature of each document, ensuring that you fully comprehend the agreements you are signing.

Consulting an attorney if necessary can provide additional clarification and guidance, especially when it comes to the financial aspects of the closing process. Comparing closing costs to the good faith estimate obtained initially can also help you identify any discrepancies and ensure you are not overpaying.

The house closing process involves a series of steps that typically take several weeks to complete, with an average timeline of 30-45 days depending on factors like home inspection and mortgage pre-approval. The two primary components of a closing are the mortgage portion and the title closing, which can have varying timelines based on the specifics of your real estate transaction.

Factors that can influence the duration of the house closing process include home inspection, mortgage pre-approval, remote closings, assuming additional debt between preapproval and closing and not being fully truthful on a mortgage application.

Being mindful of these factors and staying organized throughout the process can help ensure a timely closing.

Before commencing a home search, gaining pre-approval is beneficial in order to ascertain the exact amount that can be spent. The amount to be saved for a down payment and additional expenses depends on the purchase price of the home; for instance, a home with a price tag of $200,000 might necessitate a $40,000 down payment.

It is important to understand the distinction between mortgage pre-approval and pre-qualification as you prepare for your home purchase. Pre-approval entails a more comprehensive examination of your finances that will display your precise upper purchase limit, whereas pre-qualification is a less formal estimate of your borrowing power.

Buying a house can come with additional costs. These closing costs can be up to 2-7% of the home's purchase price and need to be paid when closing the deal. These costs are typically shared between the buyer and seller. The buyer is responsible for fees such as the initial homeowner's insurance premium which may be approximately 3 or 4% of the home's price.

For an average home priced at $300,000, closing costs may exceed $10,000. A net sheet is a document that outlines the closing costs, providing buyers with a clear understanding of the fees they will be responsible for at closing.

It is possible to withdraw from a home purchase at any time for any reason, but this may result in forfeiture of earnest money and legal issues. Commonly accepted reasons for withdrawing from a home purchase include difficulties with financing, issues arising from inspection, personal circumstances, and appraisals that come in under the expected value.

Including a home inspection contingency and a financing contingency in the home purchase can provide buyers with the necessary protection in the event that they need to back out of the deal. If you feel uncertain about your rights or require legal counsel, it is advisable to seek professional assistance.

In conclusion, closing on a house involves navigating a complex series of steps, from preparing for closing to understanding and signing closing documents. By understanding each stage of the process and following the guidance provided in this comprehensive guide, you can successfully close on your dream home with confidence and ease.

The four steps in the closing process in order are: negotiating closing costs, opening an escrow account, hiring an attorney and getting a home inspection.

Finally, lock in your interest rate and conduct a title search and insurance for added protection.

A closing walkthrough is an important part of the home buying process, allowing a buyer to assess the condition of the property one last time before finalizing the purchase. The buyer and their agent will examine all elements of the home that are included in the sale, from systems and appliances to damage and cleanliness, to ensure the home meets expectations before finalizing the deal.

This walkthrough should be thorough and comprehensive, and the buyer should take the time to ask questions and make sure they understand the condition of the home before signing the contract. The buyer should also take the time to inspect the home for any potential issues.

The closing process for the seller involves signing paperwork to finalize the sale, cleaning the property, removing possessions not included in the sale, and handing over the keys. The escrow officer will then pay off the lender and lien holders, disperse the sale proceeds to the seller, and transfer documents to the buyer.

Finally, the deed and any mortgages will be placed for recording with the county recorder of deeds.

Finalizing the purchase of a home is a major life event, and preparing for closing helps to ensure the process goes as smoothly as possible. Ensuring you have your mortgage pre-approval in order, opening an escrow account and being familiar with all the documents associated with closing are all important steps to take prior to closing on a house.

It is also important to be aware of the closing costs associated with the purchase of a home. These costs can include title insurance, appraisal fees, and other fees associated with the loan. Knowing what to expect ahead of time can help.

A title search is an important part of any real estate transaction, as it verifies ownership and potential claims against the property. Title insurance offers protection from any financial losses that may arise due to possible title defects.

| Next | 1-10 of 17 |

407-575-5392

Wendy Morris LLC

Licensed in the State of Florida

BK 3146762

16797 Broadwater Avenue

Winter Garden, Florida 34787